Understanding Medicare Basics – Why Knowing the Parts Matters

“Why do I need to understand all these different parts of Medicare?” is a question you may be asking yourself. It’s a reasonable query. Medicare is not a single, straightforward program; rather, it is composed of multiple components, each of which covers a variety of healthcare services.

Making informed decisions regarding your health coverage is aided by being aware of what Parts A, B, C, and D cover. Knowing which tools to use for each task is similar to having a toolbox.

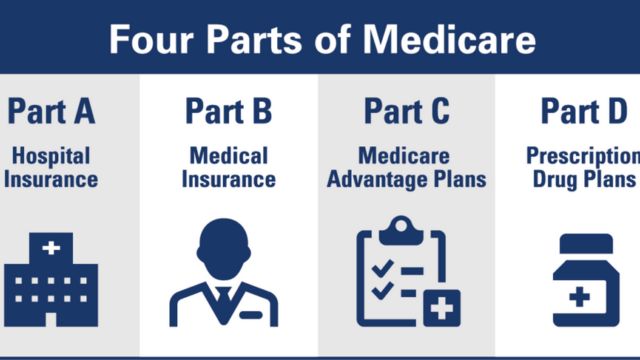

For instance, Part B deals with doctor visits and outpatient services, whereas Part A concentrates on hospital care. Medicare Advantage, or Part C, combines a number of benefits, and Part D handles prescription medication.

You risk missing out on benefits or paying more than necessary if you don’t understand what each component does. Knowing these components also helps you feel more at ease because you’ll know what’s covered in the event that you require medical attention. According to the Social Security Administration, there are four parts of medicare.

What Hospital Insurance Covers Under Medicare Part A

“What exactly does Medicare Part A cover?” is a question you may have. Excellent query!

Consider Part A to be your health insurance. If you must remain in the hospital as an inpatient, it helps with the expenses. A semi-private room, meals, general nursing care, and other hospital services and supplies are all included in this.

That’s not all, though. Hospice care in the event of a terminal illness, skilled nursing facility care following a hospital stay, and certain home health care services are also covered under Part A.

Because you or your spouse paid Medicare taxes while you were employed, most people do not have to pay a monthly premium for Part A. However, for some services, you might be required to pay coinsurance and deductibles.

You won’t be surprised by the costs if you ever need hospital care if you know what Part A covers.

Medicare Part B: Covered Medical Benefits

Let’s now discuss Medicare Part B. “What does Part B cover that is different from Part A?” you might wonder.

Your medical insurance, known as Part B, covers services you receive outside of a hospital. Preventive services like flu shots and screenings, doctor visits, outpatient care, and some home health care are included in this.

Additionally, it covers durable medical equipment, such as oxygen equipment, walkers, and wheelchairs.

The majority of people pay the monthly premium for Part B, which is typically deducted from their Social Security checks, in contrast to Part A. In addition, there will typically be a co-payment for services and a deductible.

Since Part B covers many of the daily medical services you’ll probably use, it’s important to understand it.

Medicare Advantage Part C: Integrating Benefits and Extras

After learning about Medicare Advantage plans, you may have asked yourself, “What is Part C, and how is it different from Original Medicare?”

An alternate method of receiving your Medicare benefits is through Medicare Part C, commonly referred to as Medicare Advantage. You receive a plan from a private insurance company that combines hospital and medical coverage together—and frequently includes additional benefits—instead of having separate coverage through Parts A and B.

Numerous Medicare Advantage plans provide benefits like vision, dental, hearing, and even fitness programs that Original Medicare does not cover. You might not require a separate Part D plan if your plan covers prescription drugs.

Remember that Original Medicare may have different rules, networks, and costs than Medicare Advantage plans. Finding a plan that works for you requires carefully weighing your options.

Therefore, if you want a more comprehensive plan with extra benefits, Part C can be a great option. However, it has its own set of factors to take into account.

Medicare Part D: An Overview of Prescription Drug Coverage

Let’s now discuss Medicare Part D, which provides coverage for prescription drugs, which are essential for the majority of us.

Medicare-approved private insurance companies offer Part D plans, which assist in paying for a number of prescription medications. You will pay less out of pocket when you pick up your prescription drugs as a result.

It’s crucial to understand that, unless it’s covered by your Medicare Advantage plan (Part C), you must enroll in Part D on your own. You should select a Part D plan that covers the medications you require because each one has a formulary, or list of approved medications.

Remember that premiums, copayments, and costs can differ from plan to plan, so it’s worthwhile to compare plans annually during open enrollment to find the one that best suits your needs.

It makes sense to have Part D coverage in order to better manage your health and shield yourself from exorbitant prescription drug costs.

How to Pick Your Ideal Medicare Parts

“How do I know which parts—A, B, C, and D—I actually need?” is a question you may be asking yourself.

Given that Medicare isn’t a one-size-fits-all program, that is a wise question. Your decision is influenced by your personal preferences, financial situation, and health requirements.

Original Medicare (Parts A and B) may be sufficient for basic medical and hospital coverage. However, keep in mind that Original Medicare does not cover prescription medications, so you would need to add Part D on your own.

Medicare Advantage (Part C) can combine hospital, medical, and frequently prescription coverage with additional benefits like dental or vision if you’d rather have a single plan.

Consider your medical history. Do you take a lot of medications? Do you frequently see specialists? Additionally, think about the monthly premium and out-of-pocket expenses you are willing to pay.

Utilizing Medicare’s online resources or speaking with a counselor who can assist you in comparing plans according to your needs is a smart idea.

Take your time and carefully consider your options because selecting the best combination can save you money and provide you with the coverage you require. According to the national Council on aging.

Where to Look for Help and Trusted Information

Medicare can be difficult to navigate, but you don’t have to do it by yourself. To help you comprehend your options and obtain the coverage that best suits your needs, there are many reliable resources available.

The first place to go is medicare.gov, the official Medicare website. It offers comprehensive explanations of every aspect of Medicare, plan finders, and simple-to-use tools.

For individualized support, you can also contact the Medicare helpline at 1-800-MEDICARE. They can help you compare plans, provide answers to your questions, and assist you with the enrollment process.

State Health Insurance Assistance Programs (SHIP), which provide Medicare beneficiaries with free, local counseling and support, are another excellent resource.

Numerous community centers and nonprofit organizations offer Medicare education sessions and individual counseling if you need more comprehensive assistance.

Keep in mind that seeking assistance from reliable sources can help you avoid future headaches, save money, and save time.

Have questions or personal stories about Medicare? Share them with our community in the comments below or visit Fame Tribute for more expert guides and helpful tips designed just for seniors.

Leave a Reply